I’m very pleased today to host my friends from Bridge the Data for a guest post. Bridge the Data was formerly know as Cost of Living reports, and I mentioned their reports in previous articles. Today, they share with us an extract from their KSA report which was published right at the end of 2015. Good reading !

*******

In this bulletin, we’re going to look at Saudi’s labour market, and how the price of oil is expected to affect employers over the coming year, with thorough economic analysis on the GCC’s largest employer; which we hope will help you with your salary adjustments and compensation and benefits decisions in 2016.

Salaries and the cost of living in KSA – Amidst cheap oil and a very stubborn government

The Kingdom of Saudi Arabia headlined in 2015 for the instability its economy faced due to a deflated world oil price (reaching as low as $35 a barrel – well below Saudi Arabia’s breakeven point of $80).

But that was not the only buzz Saudi Arabia generated.

As the global energy sector lost jobs, assets and cut back on production to salvage costs, Saudi Arabia insisted on not cutting back its output, in fact, the Kingdom’s publicly funded energy firm Aramco invited talent from Western economies to join its labour force in KSA, during downward economic times. Spectators and speculators argued that the Kingdom would not be able to withhold the losses any further, and that a decline in output was necessary.

Our research team was then faced with the task of analysing whether there were in fact job losses in Saudi’s energy sector, the impact of cheap oil on salaries, and to try and get a glimpse of the future – If at all possible.

The total number of oil & gas job losses globally was at 150,000 in June 2015, according to global oilfield staffing firm Swift Worldwide Resources. While global exploration and production companies relied on cutting back payroll, contracts and whatever expenses they could spare to survive, Saudi Arabia announced that its plan to reduce a budget deficit of over USD 98 billion would be to reform energy subsidies and begin an even stronger privatisation drive – without reducing its oil output.

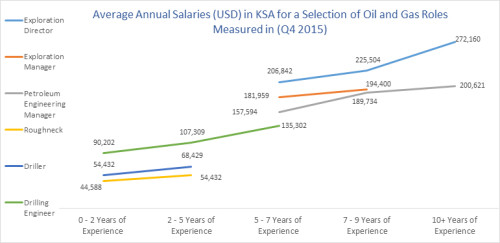

But have there actually been job cuts? Where are these job cuts saturated, and how were salaries in 2015 impacted (a sample of the reported salaries in our Cost of Living KSA Report is shown below)? Have there been any gains in salaries, in any sectors, and how has the cost of accommodation, education and healthcare adjusted to changes in the supply and demand of labour?

Note – Sample taken from the Job Market section of Bridge The Data’s 2015/ 2016 Cost of Living KSA Report, released in December 2015.

If we look more closely at Saudi’s oil output strategy, what we can deduce is that Saudi Arabia has been flooding the market with cheap crude, in an effort to drive its high-cost competitors out of business – but perhaps that isn’t as simple as it has been in the past. Shale drillers can stay profitable at lower prices than before, and more importantly, can turn production on or off as needed, for relatively little expense. So is the Kingdom really as immune to low global oil prices as it claims to be?

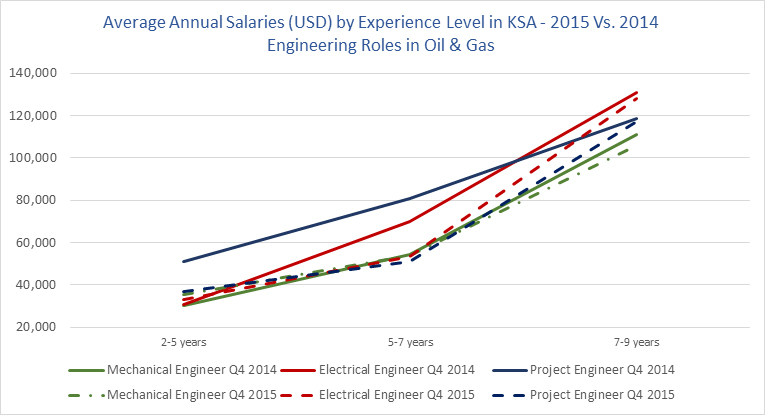

The truth is, probably not….. Being impervious to such circumstances is a near on impossibility, and as a result, the energy sector in Saudi Arabia has made substantial cuts. One indicator of this is the freeze in earning gains witnessed in the energy sector during 2015.

The graph below is extracted from the Salary Benchmarking section of our Cost of Living KSA Report, and shows the average change in earnings for a selection of roles in the energy and engineering sectors over time.

Please click here to see the 2015/ 2016 Cost of Living KSA Report’s table of contents

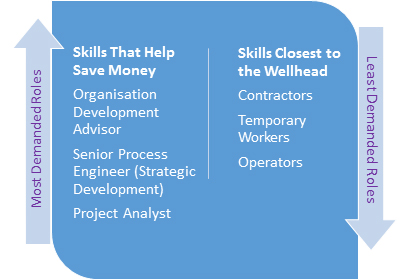

Since mid-2015, hiring practises have been more focussed on the talent that saves money. Occupations that analyse processes and recommend cost saving improvements are highest in demand, whilst roles closest to the wellhead are most in threat. In addition, hard bargaining with contractors has led to job losses at the bottom of the food chain (the closer to the wellhead, the bigger the losses.)

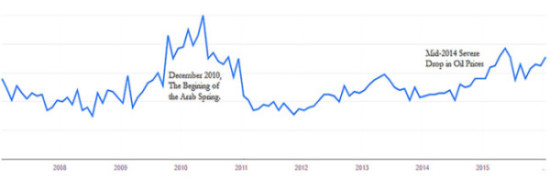

Google Trends’ two cents on Saudi’s labour market in 2015

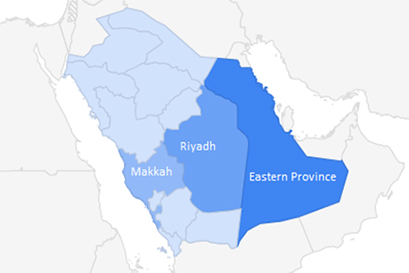

Geographic Regions Within KSA with the Highest Search for Jobs Online

Our analysts have used the publicly-available data on Google Trends to graph the frequency of job searches from within Saudi Arabia over time. The graph we generated is below.

A spike in job search arises in late 2010, as the Arab Spring begins. Several individuals have fled their home countries seeking employment in other more stable nations.

By Mid-2012, as the GCC countries tighten their borders from a potential influx of refugees a decline in search intensity is apparent.

The next time the search intensity spikes again is in Mid-2015, when the oil price fell from $110 to $50 in early 2015. In addition, a major part of the search seems to be generated by users in the Eastern Province, where most oil firms reside.

Google Searches for Job Search Keywords from Within Saudi Arabia Over Time

Data on salaries and the cost of living

The Cost of Living KSA Report 2015/ 2016 is a valuable source of intelligence for firms looking to appropriately resize budgets and readjust allowances which reflect the actual market climate in KSA, rather than simply mimicking the competition. With 10+ years of data and trends in the Middle East, our reports, both quantitative & qualitative, provide insight into the socioeconomic, political & legislative reforms, for the UAE, Qatar, KSA and rest of the GCC, as well as Egypt & Iran.

********

About the authors :

Bridge The Data has over 12 years of data, 40 individual reports on the cost of living, in 30 cities throughout the MENA region, and has been helping more than 50 Fortune 500 clients make sound compensation and benefits decisions, each financial year. You can reach them at info@bridgethedata.com or call them at +971 4409 6838.

Full disclosure : If you decide that you like what you read, and buy a report from Bridge the Data, I will earn a small commission on it if you mention that you were introduced by Compensation Insider / Sandrine Bardot. Given that the price of the report is very decent, I obviously won’t become super rich in the process, but this will be an encouragement for me that indeed, the products and services I recommend are useful to my community. So go check them out !

Copyright secured by Digiprove © 2016-2017 Sandrine Bardot

Copyright secured by Digiprove © 2016-2017 Sandrine Bardot

Good read… I tend to like clarity on one point. I have come across articles that state shale producers would find the present price range to be tough sustaining their production. Secondly the shale producers have invested hugely at the time the prices reached their zenith. This means that at present times, with the prices at it low, it would be difficult for them to sustain. So can shale producers stay alive?

But thanks for sharing the information.

Thanks for your comment Philip. As you know, on this blog we focus on topics related to Compensation & Benefits, Performance Management and HR in general. I’m not an expert on oil prices, and my partners Bridge the Data focus on collecting, analysing and synthetising information which will bring context and background for the decision-making process in HR, so probably not best placed either to comment on that specific aspect. If some of the readers have opinions or specific knowledge on shale producers and how they can survive these times of low prices, I’ll be happy to learn from them in their comments though !

Hi Philip,

Interesting point. Shale oil producers are certainly suffering but they are in my opinion far more flexible than huge operations in the GCC. Here is a link to a blog post on the World Bank’s site about it

http://blogs.worldbank.org/prospects/global-weekly-flexibility-us-shale-oil-industry

KSA is certainly hoping that the price will decline by enough to have the shale producers go bankrupt, leaving a much smaller group of producers globally and a high and sustainable price. But its been over a year now, and observational statistics have shown that these shale producers shut operations down quickly when the price is low and re join the market when its high again! In addition, shale producers are investing in technology to lower extraction costs.

I saw an interview by a Muhammed bin Salman (KSA’s second man) with The Economist magazine a few month back. Their strategy seems to have changed. Instead of playing a game of waiting for shale producers to go bust, they are seeking to raise capital for ARAMCO publicly and begin financing the mining industry. In my mind, there new strategy seemed to be indicating how difficult it is to completely eliminate shale producers in the long term.

Thanks Engy (from Bridge the Data) for bringing some interesting facts to the discussion ! I have also read that over the long run, only a few countries, mostly in the GCC, can afford low oil prices because their production costs are the lowest. The article pointed that the countries really suffering are such as Nigeria, Venezuela (both OPEC members) and Argentina (admittedly, a shale not oil producer and non OPEC member).